Executive Summary

Prepared by Avery Schwartz, Raz Mangel and Lior Sulkin-Levy

Scroll down to view the report in article form, or feel free to download the report via the 'pop-out button' below

As we have seen since the beginning of 2022, the economic situation in the US and Europe is rapidly changing, with inflation peaking near record levels and the US Federal Reserve hiking interest rates quickly and dramatically in response. These macro factors, which are also affected by the geopolitical situations in the world, are dramatically affecting technology companies and startups. While we do not specialize in the macro climate, we wanted to provide the ecosystem with a summary of the key macroeconomic metrics that are rapidly changing. We believe that investors and founders should be aware of these changes and apply first principles to try and understand the effects it might have on their businesses.

- As a reminder, we recently published in our Q2inReview report, a compilation of all capital raises within Israel’s tech ecosystem, insights into the state of the venture market, and started seeing some slowdown in the Israeli venture market, which is correlated to the macroeconomics effects that we will discuss in this report

- Inflation remained high last month (July 2022) at 8.5%, after peaking at 9.1% in June

- The 9.1% peak represents a 40+ year high

- The Fed funds effective rate is 2.33%, and forward markets anticipate a rise to 3.40% by the end of the year. In the recent Jackson Hole meeting, the Fed has announced that they are planning to keep playing on the aggressive side to do whatever it takes to bring down inflation to their 2% YoY target

- Narrow technical recession has set in given negative GDP growth in Q2 2022 of (0.9)%, following a (1.6)% drop in Q1 2022

- Atlanta Fed (GDPNow) is predicting 1.4% growth in GDP for Q3 2022

- The US housing market has not yet been broadly affected, but is most likely on a correction course due to the rise in interest rates and stagnant economy; we could expect a decline in housing pricing (in some areas in the US)

- Brent crude is still relatively elevated, but at ~$100 is ~18% off its recent high of $122

- Consumer Confidence Index (CCI) and Purchasing Managers Index (PMI) are on the decline, both are indicators to the growth and strength of the economy

- PMI is hitting 2 years low, but remains above 50 and still above pre-COVID levels

- PMI is hitting 2 years low, but remains above 50 and still above pre-COVID levels

- Unemployment remains at an all-time low territory at 3.6%, but participation rate has fallen off slightly for the first time since Covid

- Bond yields have spiked since the beginning of 2022; however, they have started to decline in recent weeks

Inflation and Interest Rates Over Time

Trend Explanations and Implications Moving Forward

Upward Inflationary Pressure

- Drivers of inflation: sharply rising labor costs, factory shutdowns, global shipping backlog, and pent-up consumer demand

- Today: consumer prices have climbed more than 8% over the past year – fastest rate of increase in 40 years

- With demand outpacing supply, inflation will continue to erode the purchasing power of consumers

- Vehicle prices up ~7%, food prices up ~10%, and energy prices up ~42% since last year

Monetary Policy Response

- The Fed is tightening monetary policy to fight inflation. Specifically, it is raising the short-term interest rate that it controls directly (aka the Fed funds rate)

- Central bank officials use this rate to slow down the economy – in this case to weaken demand so that supply can catch up

- Most recently, the Fed raised interest rates another 0.75% to about 2.25% to 2.50%.

- In addition, the fed communicated that they would remain aggressive with interest rate raise in order to bringdown inflation to their 2% yearly target

- Because higher interest rates mean higher borrowing costs, people will eventually start spending less. Ideally, the demand for goods and services will drop and cause inflation to slowdown

- By increasing the federal funds rate, the Fed is effectively trying to shrink the supply of money available for making purchases

Looking Ahead

- The benchmark interest rate will likely end the year around 3.4% and around 3.8% in 2023

- The Fed is seeking to raise interest rates enough to curb inflation without causing a recession—a so-called soft landing

- The risk is that demand falls too much, which could lead companies to cut production and layoff employees, pushing the economy into a recession

Real GDP Overview

Trend Explanations and Implications Moving Forward

Cooling Economic Growth

- The upward growth trajectory in the U.S. was disrupted when real GDP fell unexpectedly by 1.6% in the first quarter of 2022 and most recently 0.9% in Q2. This occurred after a nearly 7% gain during the previous quarter, prompting forecasters to lower growth projections for 2022 and 2023

- Factors that have contributed to declines in GDP: sizable decreases in real net exports and inventory investment ▶ combined to subtract 4 percentage points from real GDP growth

- On the bright side, personal consumption expenditures and nonresidential (business) and residential fixed investment combined to account for over 3 percentage points of real growth

Looking Ahead

- Economic growth seems to continue to cool throughout 2022

- Some of the reasons for the last two quarters decline in Real GDP Growth include high inflation and rapid monetary tightening, which curb consumption and business investment growth

- The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2022 is 1.4%

Housing Market Trends

Trend Explanations and Implications Moving Forward

Housing Prices Since ‘08 Crisis

- The housing market has generally recovered. Although prices fell 33% during the Great Recession, they have rebounded and are now up more than 50% since hitting the bottom of the market

- The housing market is entering a new phase: homes are more available, buyers may be more scarce, and certain sellers may not want to put their houses on the market

- Home prices have soared largely due to inflation, low supply, and pandemic-fueled demand over the past two years

- The median selling price for existing homes stands on $403,800 after reached a record high of $413,800 in June

Recently Falling Starts

- Housing starts in the U.S. dropped 7.25% month-over-month to an annualized rate of 1.446 million units in July 2022, the lowest figure since February of last year

- The housing sector has been cooling due to soaring prices and mortgage rates

- Single-family housing starts sank 8.1% to 982,000 while starts for units in buildings with five units or more came in at 568,000

- Sustained declines in housing starts often serve as a sign that the economy is slowing down and a recession may be imminent

Looking Ahead

- The nation’s housing market might be on a correction course:

- Rising interest rates and a stagnant economy are already diminishing the rapid home-price appreciation the housing market has experienced over the past year

- Several economists predict the deceleration in home prices will continue as homebuyer demand wanes

- As the Federal Reserve continues to take aggressive actions to curb inflation, mortgage rates will likely rise further, crushing affordability and curbing demand within the housing market. As a result, it’s predicted that inventory will continue to increase, housing deals will fall through, and some sellers might have to reduce prices

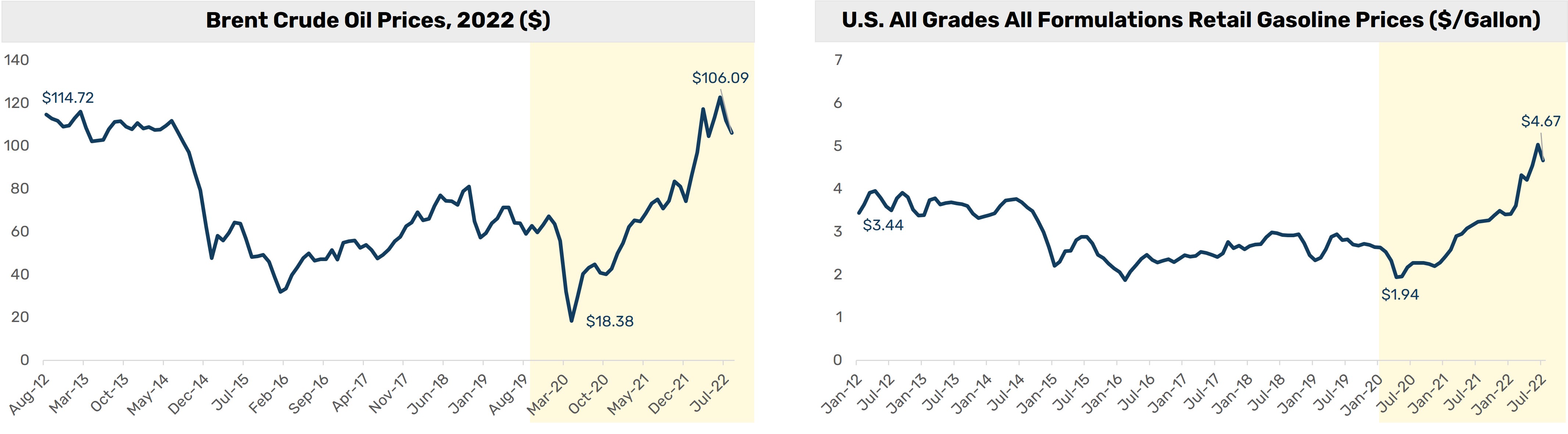

Oil and Gas Price Trends

Trend Explanations and Implications Moving Forward

Fluctuations in Oil Prices

Business Today

“Oil futures have been volatile in recent weeks as traders try to reconcile the possibilities of further interest rate hikes that could limit economic activity, and thus cut fuel demand growth, against tight supply from the disruptions in the trading of Russian barrels because of the Western sanctions amid the Ukraine conflict.”

Post-COVID Pain at the Pump

- High demand for crude oil and low supply pushed gas prices upward earlier this year by almost 50%, reaching $5/gallon nationwide

- The biggest driver of the cost of gas had been the price of crude oil, which hovered around $120 a barrel in June

- However, drivers have received some much-needed financial relief at the pump, as gas prices have been trending downward for more than 50 consecutive days. The average cost of a gallon of gas down almost a dollar since the June peak

- Gas prices have been declining for several reasons, including an increase in gasoline production and a decrease in the cost of crude oil. Recession fears have also knocked down prices

Looking Ahead

- High oil and gas prices are likely here to stay

- The West’s sanctions against Russia will yield insufficient alternatives, given that Russia accounted for 14% of global oil supply last year

- Although soaring inflation and sluggish growth raise the likelihood of recession, global demand for oil is unlikely to fall enough to dent prices, as it did in 2008

- As the Chinese government unwinds COVID-19 restrictions, pent up demand could push up prices. Demand in the U.S. has also remained resilient despite high prices

- The upcoming winter in Europe and the U.S. is likely to increase the demand

- Another broader factor is the hesitancy of U.S. producers to spend big money on extracting and refining fossil fuels given the widespread shift to renewable energy

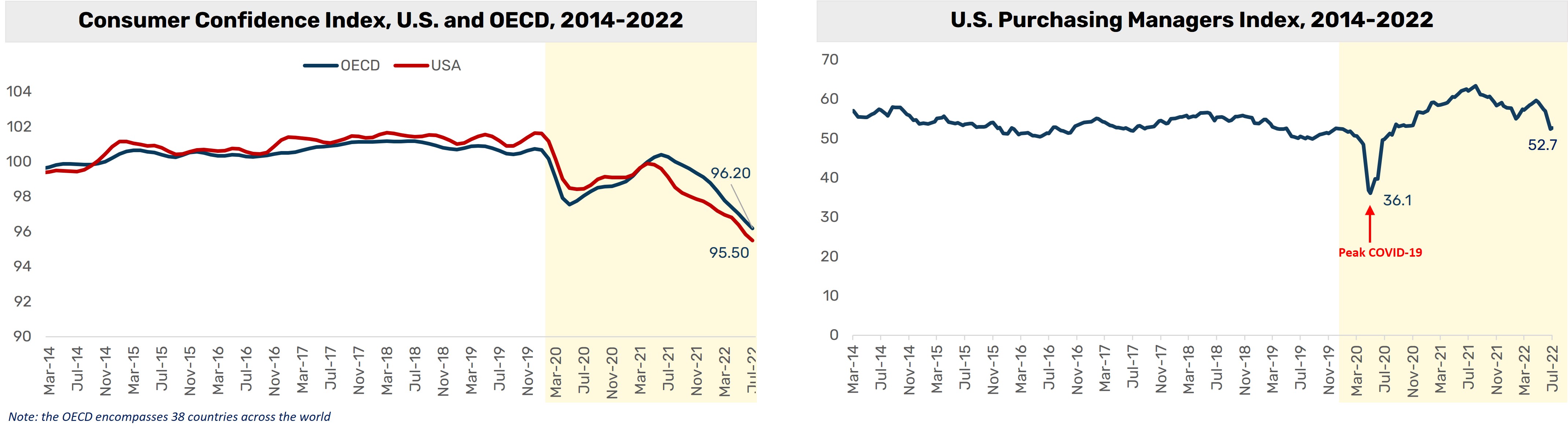

Consumer Confidence & Purchasing Managers Indices

Trend Explanations and Implications Moving Forward

Diminishing Consumer Confidence

- This consumer confidence index provides an indication of future developments of households’ consumption and saving

- The current values below 100 indicate a pessimistic attitude towards future developments in the economy, possibly resulting in a tendency to save more and consume less

- From a macro perspective, rising inflation has clearly weighed on consumers’ purchasing power by slowing gains in real wages and wealth

- Interest rate hikes have further incentivized consumers to save dollars that can earn higher interest rates rather than spend their money

Decelerating Expansion

- The PMI index summarizes economic activity in the manufacturing sector

- A PMI over 50 represents growth or expansion in comparison to the previous month, while a reading under 50 represents contraction in the manufacturing sector of the economy

- US Manufacturing PMI is at a current level of ~52, down from ~57 in June and down from ~63 one year ago. This represents a change of -8.5% within two months and -17.5% from one year ago

- Thus, the manufacturing sector of the economy seems to still be expanding but at a slower rate, likely due to the lasting impact of COVID-19 as well as ongoing supply chain hurdles

Looking Ahead

- After recent news that the Consumer Confidence hit a 16-month low, it appears that consumer confidence will continue to decline as dimmer views of the economy, inflation, and rate hikes persist

- Some experts claim that “there will only be a sustainable trend shift in consumer sentiment if there are successful peace negotiations on the war in Ukraine”

- Surveys reveal that consumers are much less likely to make big purchases like cars, vacations, and major appliances over the next six months

Employment Statistics

Trend Explanations and Implications Moving Forward

A Glimmer of Economic Hope

- Total employment rose by 242,000 in July, and the unemployment rate remained at 3.5%.

- The U.S. economy experienced extensive hiring throughout June, helping to try and steer the US from recession even as inflation eats into wages and interest rates continually rise

- Hiring has persisted even in industries vulnerable to interest-rate increases and shifting consumer habits

- For example, construction firms, susceptible to a faltering housing market and higher mortgage rates, added jobs last month

- Broadly speaking, unemployment negatively impacts the disposable income of families, erodes purchasing power, and reduces an economy’s overall output

Slowly Recovering Participation

- The labor force participation rate estimates an economy’s active workforce by dividing the number of people aged 16 and older (who are employed or actively seeking employment) by the total population

- The portion of the population that is working or looking for work remains 1.2 percentage points below their February 2020 values, as Americans that left work during the pandemic are gradually returning to the workforce

Looking Ahead

- As the Fed is taking stronger action to fight inflation, the economy could be taking another step towards a recession that could lead to a hiring slowdown and rising unemployment

- However, the strong labor market continues to represent a sliver of hope when it comes to avoiding some of the devastating implications of a recession

- While a downturn is obviously inevitable, the labor market remains red hot in the U.S., a sign of strength during devastating macroeconomic times

- However, low unemployment rate might cause inflation to remain high for several years

High Yield & Investment Grade Indices

Trend Explanations and Implications Moving Forward

Growing Bond Risk

- This index tracks the performance of U.S. dollar denominated below investment grade corporate debt publicly issued in the U.S. domestic market

- Essentially, the recent upward trend in the index means that investors are asking for higher interest rates to compensate for the greater risk of investing in corporate bonds

- Companies with lower credit ratings are often at a higher risk of default during distressing macroeconomic circumstances

- Risk-averse sentiment has largely been driven by the geopolitical crisis in Ukraine, global inflationary pressures, and the growing aspects of a potential recession

Investment Grade

- This index tracks the total return anticipated on a bond if the bond is held to maturity

- Yield to maturity is expressed as an annual rate regardless of the bond's term to maturity

- The growing yield is directly correlated with the Fed’s increase of the US interest rate to fight inflation

- The steepness of the rise in IG yields can indicate how deep the market expects the recession to cut, i.e., to what degree investment grade issuers will be suspected of potential default

Looking Ahead

- Bonds are considered to be a safer alternative to stocks, which might cause investors to turn to bonds if the recession will continue but the expected increase in interest rate is adding weight on bonds performance

- High Yield - bond index increases in recessions – the highest measure was 23% in November 2008 at the financial crisis. Therefore, if the recession will continue, we expect to see the index increasing as risks of defaults surge

---------

Report prepared by Avery Schwartz, Raz Mangel, Lior Sulkin-Levy, and Isaac Goldman

Disclaimer

General Disclaimer

This presentation (the "Presentation") is provided for informational purposes and reference only and is not intended to be, and must not be, taken as the basis of an investment decision. These materials include internal data and/or analysis used by Greenfield Partners Investment Management Ltd. (together with its affiliates, "Greenfield"). By acceptance hereof, you agree that (i) the information contained herein may not be used, reproduced or distributed to others, in whole or in part, for any other purpose without the prior written consent of Greenfield; (ii) the information contained herein is confidential and subject to the restrictions and you will keep confidential all information contained herein not already in the public domain; (iii) the information contains highly confidential and proprietary “trade secrets” (some of which may constitute material non‐public information); and (iv) you will only use the information contained in this Presentation for informational purposes and will not trade in securities on the basis of any such information. By acceptance hereof, you also agree that (i) you are (a) a bank, savings and loan association, insurance company or registered investment company, (b) a federal or state registered investment adviser or (c) a person (including a natural person, corporation, partnership or trust) with total assets of at least $50 million and (ii) you are capable of independently evaluating the investment risks of a potential investment in any Greenfield sponsored investment fund (the “Fund”) and will exercise such independent judgment in evaluating a potential investment in the Fund.

The contents hereof should not be construed as investment, legal, tax or other advice and you should consult your own advisers as to legal, business, tax and other related matters concerning an investment in the Fund. This Presentation does not constitute an offer to sell or a solicitation of an offer to buy any securities and may not be used or relied upon in evaluating the merit of investing in the Fund. A confidential private placement memorandum (including any supplements thereto, the “PPM”) and other definitive documentation relating to the Fund or your investments therein, including constitutive documents and subscription documents (collectively, the “Fund Documents”), will be made available and must be received by you prior to subscribing for an interest in the Fund. An offer or solicitation for the Fund will be made only through the PPM, which will contain additional information regarding the Fund. The information set forth herein is not part of or supplemental to the PPM, the Fund Documents or any documents ancillary thereto. The information set forth herein will be superseded in its entirety by the PPM and the Fund Documents. In the case of any discrepancy between the information contained herein and the PPM or the Fund Documents, the PPM and the Fund Documents will control.

No representation or warranty, express or implied, is given in respect of the information contained herein (including its accuracy and completeness). All information contained herein has been compiled as of the date this Presentation is made (or as otherwise specified), and there is no obligation to update the information. Neither the delivery of this Presentation nor the placing of any interests in the Fund will under any circumstances create any implication that the information herein has been updated or corrected as of any time subsequent to the date of publication or, as the case may be, the date as of which such information is stated. Information throughout the Presentation provided by sources other than Greenfield has not been independently verified. Differences between past performance and actual results may be material and adverse.

Any projections, estimates, forecasts, targets, prospects, returns and/or opinions contained in these materials involve elements of subjective judgment and analysis and are based upon the best judgment of Greenfield as of the date of these materials. Greenfield does not take responsibility for such projections, estimates, forecasts, targets, prospects, returns and/or opinions. Any valuations, forecasts, targets, opinions and projections expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.

An investment in the Fund is speculative and involves significant risks, including that there will be no public or private market for the interests in the Fund and such interests will not be transferable without consent as set forth in the Fund Documents. Investors should understand these risks and have the financial ability and willingness to accept them for an extended period of time before making an investment.

Please note this Presentation contains various examples of investments. There is no assurance that any investments discussed herein will remain in the applicable fund at the time you receive this information. It should not be assumed that any investment not shown would perform similarly to the examples shown. It should not be assumed that recommendations made in the future will be profitable, will equal the performance of the investments in this Presentation, or will not incur losses. Future investments may be under materially different economic conditions, including interest rates, market trends and general business conditions, affecting different investments and using different investment strategies and these differences may have a significant effect on the results portrayed. Each of these material market or economic conditions may or may not be repeated. Further investments may be made under different economic conditions, using different strategies, and may have materially different results. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the investments in this Presentation. Past performance is not necessarily indicative of future results. Differences between past performance and actual results may be material and adverse. Investments made in the future may not be profitable or may not equal the performance of the investments described in this presentation. Gross performance results, including value created and realizations, do not reflect the deduction of investment advisory fees, expenses and carried interest. Actual returns will be reduced by these fees.

Forward Looking Statements

All statements in this Presentation (and oral statements made regarding the subjects of this presentation) other than historical facts are forward‐looking statements, which rely on a number of estimates, projections and assumptions concerning future events. Such statements are also subject to a number of uncertainties and factors outside Greenfield’s control. Such factors include, but are not limited to, uncertainty regarding and changes in global economic or market conditions, including those affecting the industries of Greenfield portfolio companies, and changes in U.S. or foreign government policies, laws, regulations and practices. Opinions expressed are current opinions as of the date of this presentation. Should Greenfield’s estimates, projections and assumptions or these other uncertainties and factors materialize in ways that Greenfield did not expect, actual results could differ materially from the forward‐looking statements in this presentation, and investors may lose a material portion of the amounts invested. While Greenfield believes the assumptions underlying these forward‐looking statements are reasonable under current circumstances, investors should bear in mind that such assumptions are inherently uncertain and subjective and that past or projected performance is not necessarily indicative of future results. No representation or warranty, express or implied, is made as to the accuracy or completeness of the information contained in this presentation, and nothing shall be relied upon as a promise or representation as to the performance of any investment. Investors are cautioned not to place undue reliance on such forward‐looking statements and should rely on their own assessment of an investment.